From crisis to resilience:

What to expect for supply chains in 2023

By Duncan Mayall

Why supply chains matter

In the last three years, supply chains have gone from a minority concern to a central issue. During the Covid-19 pandemic, we saw the damage caused when supply chains fail to function – absence of key medical supplies, risks to food security and, when bottlenecks emerged in 2021, rising inflation and risks to companies’ ability to operate.

Building up greater resilience to reduce the risk of these challenges emerging again remains vitally important.

And alongside these short-term changes to global supply chains are much broader longer-term trends that are reshaping how and where goods are made.

The world is changing – what made economies competitive in the past will not necessarily make them competitive in the years to come. For some countries, the rise of automation and a low-carbon economy are a threat to important entrenched industries – for others, they are an opportunity to expand their share of global production.

Finally, there is much more that countries can do to maximise the impact of the links that they already have with global production chains – both the operations taking place within their borders and the lessons being learned by their own companies operating overseas.

This report looks into the trends that have shaped these issues in recent years, what is likely to shape them in the years to come, and explores the research into what governments can do to position themselves for success.

Supply chain issues have had a significant impact

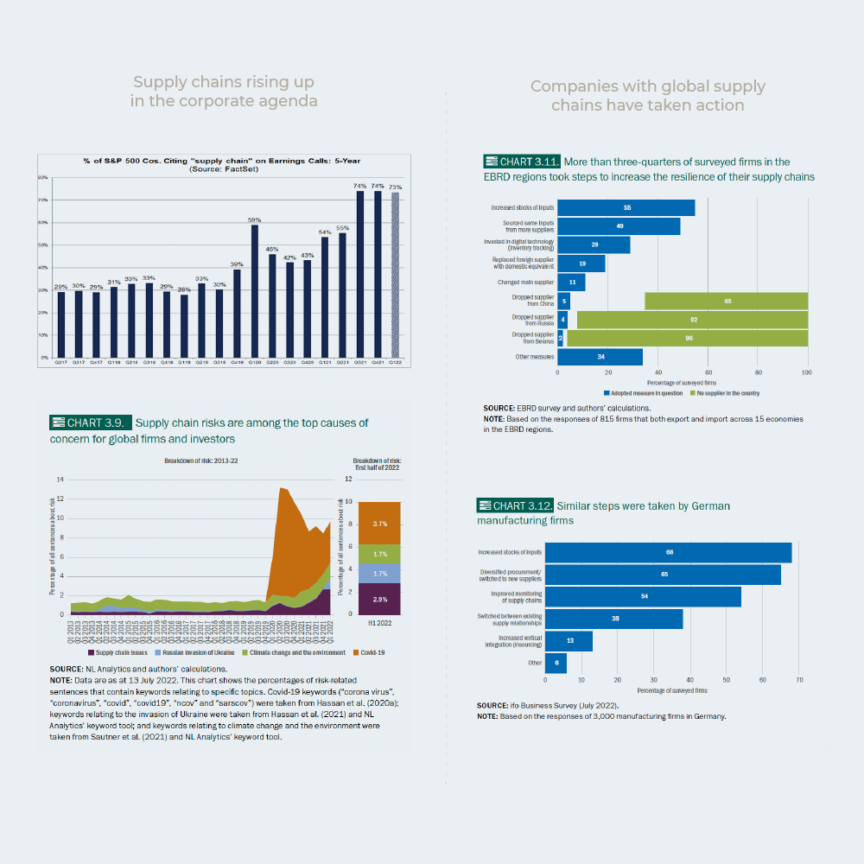

It is perhaps no surprise that ‘supply chains’ were one of the most frequently mentioned issues in corporate earnings calls in 2022. Companies from furniture makers to car manufacturers cited supply chain issues as driving major financial stress.

Leaders are taking action to increase their resilience, with a recent EBRD survey* finding that more than three-quarters of firms have implemented at least one measure aimed at strengthening the resilience of their supply chains.

While the most popular measure was to increase stocks, nearly 50 percent of those surveyed said they were sourcing inputs from more suppliers and nearly 20 percent had replaced a foreign supplier with a domestic equivalent.

Likewise, in December 2022, the GEP Global Supply Chain Volatility Index saw a notable increase in firms’ safety stockpiling amid concerns rising cases of Covid-19 in China – companies are now responding quickly to potential risks in their supply chains.

*Transition Report 2022-23, European Bank for Reconstruction and Development, November 2022

Some prominent pressures have eased

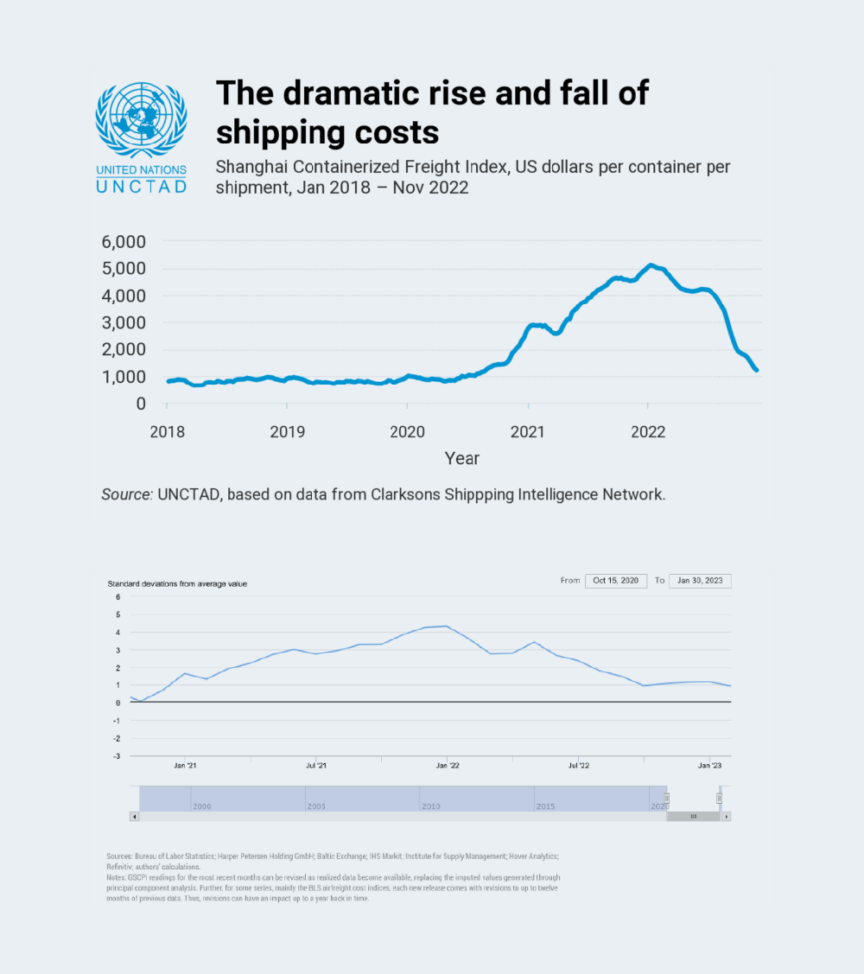

Two of the most prominent pressures on global supply chains following concerns about medical equipment in the initial phase of the pandemic – were the ease and cost of transporting goods and the availability of semiconductor chips.

In both cases, there is growing evidence that these pressures have now passed. Shipping bottlenecks appear to have reduced and costs have fallen considerably on the back of lower demand.

Likewise, after a period of high demand and a shortage of chips, several major manufacturers have announced reductions in output as demand reduces.

More broadly, indicators of supply chain volatility have pointed to the system becoming much less strained. For example, the GEP Global Supply Chain Volatility Index, which had peaked above 6 in late 2021, fell below 1 in January 2023 – its lowest reading in more than two years. Many other measurements, such as the Federal Reserve Bank of New York’s Global Supply Chain Pressure Index, tell a similar story.

That is not to say that there is zero risk. An unexpectedly robust recovery across developed markets could drive a restocking surge at the same time as as demand grows with the reopening of the Chinese economy..

Supply bottlenecks could re-emerge, too, whether driven by further waves of Covid infections in China or by unresolved labour disputes in the US west coast ports, affecting more than 20,000 workers at some of the country’s key entrance points.

However, for the moment at least, it seems likely that these concerns will no longer be front of mind in the way they have been.

Focus is likely to shift from crisis to resilience

As near-term, headline-grabbing pressures recede and focus moves elsewhere, we anticipate that the debate around supply chains and global value chains may become less prominent.

However, while it may fade from the headlines to some degree, it is likely that the requirement to strengthen long-term resilience will mean that supply chains remain a pertinent issue. And, as the recent jump in safety stockpiling demonstrates, companies remain highly sensitive to the potential risks.

Furthermore, supply chain resilience is increasingly tied not only to physical disruptions but to a broader increase in protectionism and geopolitical tension. These factors are unlikely to recede in the near term and so it is likely that where goods are made will continue to be a focal point for discussion.. Supply chains, like foreign investment, are increasingly being seen as a matter of national security. This is particularly (though not exclusively) the case with industries linked to ‘dual-use’ technologies such as the production of advanced semiconductor chips.

As a result, non-economic concerns will play a more important role in determining where goods are produced.

Friend-shoring has already emerged as a potential solution – being promoted by US Treasury Secretary Janet Yellen, among others. On the one hand, friend-shoring has the advantage of offering firms some of the advantages of reshoring (reducing geopolitical risk, diversifying supply chains) while maintaining what is likely to be a more competitive cost of production.

On the other hand, ‘friendship’ can be a complicated concept to apply in geopolitics. Implicit in the term ‘friend-shoring’ is that countries can only be ‘friends’ with one group. This is likely to pose challenges for those nations and companies looking to preserve working ties with countries that increasingly see their interests as conflicting.

Over the last three years, the debate around supply chains has been framed around the trade off between resilience and efficiency. Absent a return to significant shortages in key goods, we expect that in the coming years, the debate will increasingly be framed around strategic competitiveness and national security.

Where global supply chains go next

While they still play a vital role in the world economy, global supply chains are changing. And the way they are changing will help to determine which countries are likely to succeed and be likely to play a more prominent role in these value chains in the future.

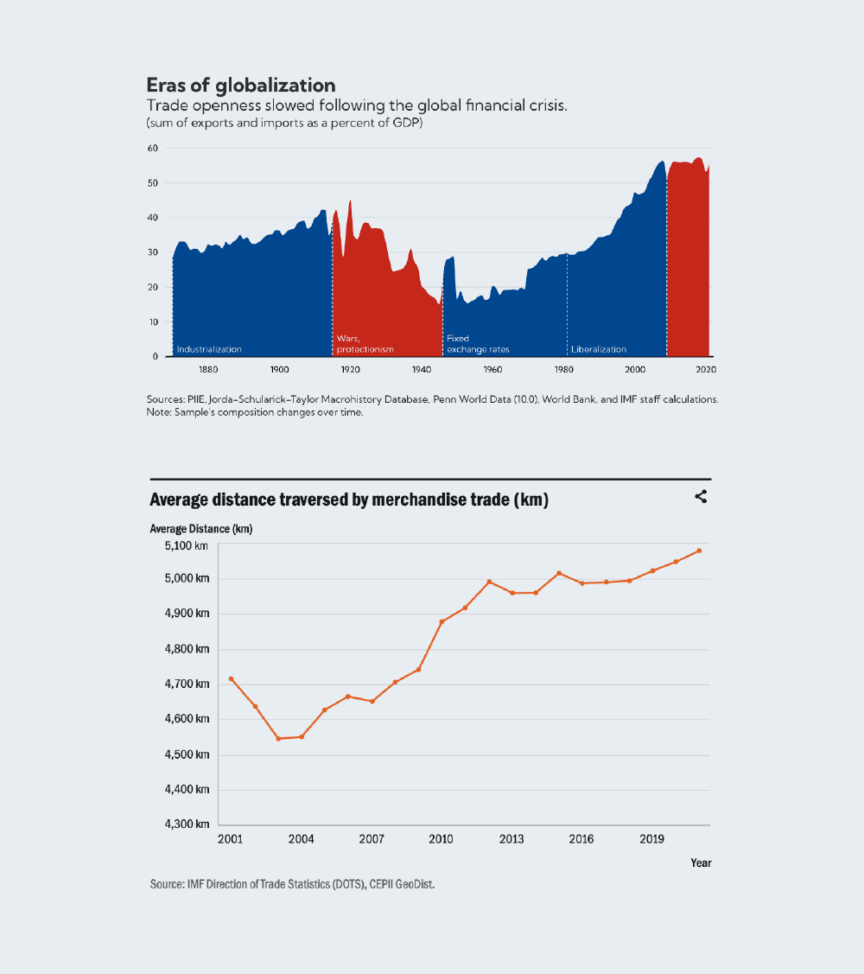

Global value chains grew rapidly in the era of globalization in the 1990s and the first half of the 2000s following the end of the Cold War and China’s accession to the World Trade Organization (WTO). However, as with foreign direct investment, there is evidence suggesting that the development of global value chains has plateaued since 2008 in line with the slowing expansion of globalisation.

In recent years there has been growing speculation about the future of global supply chains, trade, and foreign direct investment, prompted by concerns that the pace of globalisation is either permanently slowing or set to go into reverse.

Analysis from UNIDO suggests that, at least so far, trade routes do not appear to be shortening – indeed, it argues that ‘trade has tended to take place over longer rather than shorter distances’. This does not, however, mean that global trade flows have been unchanged – nor that they will continue to shift towards a greater reliance on Asia, which UNIDO identifies as the key driver of the shift.

It is important to remember that supply chains are much more elastic in the long term than they are in the short term. Koenig and Poncet (2022) found that after the collapse of the Rana Plaza building in 2013, there was a relative decline in Bangladeshi imports for those French retailers named for sourcing from the collapsed factories. This effect was mirrored by a relative increase in these exposed firms’ imports from four particular countries, which are non-Asian and geographically closer to France. In other words, when faced with a potential reputational threat, firms were willing to relocate production to higher-cost locations.

If the world is no longer organised in the way that it used to be, with much greater geopolitical fragmentation and a range of new global challenges, then multinational companies’ value chains seem likely to adapt accordingly.

Key trends driving significant change to global supply chains

In this section we look at three key trends that have the potential to drive significant changes to global supply chains – assessing how this is likely to influence the narrative around them and what the potential implications could be.

However, it is worth remembering one important caveat: Restructuring supply chains and trading off some efficiency in favour of resilience or security is likely to come at a cost. The extent to which consumers are willing to accept higher prices – or firms to accept tighter margins or a less efficient capital allocation – has not yet been fully tested. For some of the answers, we will need to wait and see.

1. The increased focus on security and resilience of supply

While the immediate pressures on supply chains following the Covid-19 pandemic appear to have subsided, the world has not returned to the status quo pre-Covid. The vulnerability of supply chains during the pandemic has focused policy makers’ attention on the resilience and, in an age of heightened geopolitical tension, the security of supply chains. This means that governments are increasingly seeing global value chains through the lens of national security rather than economic efficiency. The debate has moved from semiconductor chip shortages to ‘chip wars’ between the US and China.

At the same time, there is some evidence to suggest that businesses are re-thinking their value chains and placing a greater emphasis on resilience and security of supply – being willing to accept higher costs and a lower level of efficiency as a result.

Exactly what this will mean in practice is not yet fully clear and is likely to vary between firms. It may lead to more regional supply chains, with goods traveling shorter distances (although UNIDO analysis suggests that this has not happened yet). It may lead to ‘friend-shoring’ as firms relocate activities to geopolitical allies. It may lead to greater diversification as firms draw on multiple sources of inputs to reduce the risk of bottlenecks.

Potential Implications:

- Strong state capacity will become an increasingly important competitive advantage in attracting investment: Countries that can demonstrate an ability to provide security and stability of operations during periods of disruption – most notably during Covid-19 – will be particularly well-placed to attract investment by positioning themselves as a resilient destination in uncertain times.

- Geographical proximity and connectivity with key markets will rise in importance: One of the key winners will be locations that are relatively close to, and have strong connections with, key markets in the overall value chain (e.g. key sources of raw materials or end markets). These locations can position themselves as enabling firms to reduce the risk of disruption of key links in the chain.

- Countries able to manage challenging geopolitical currents will emerge as winners: Countries that are subject to a comparatively low level of geopolitical risk and which are able to maintain a geopolitical posture which maintains a level of access to key markets for companies operating there will be best placed to continue to thrive.

2. Technological advances and the growth of automation

Rapid technological advancement – particularly within automation – is disrupting a number of industries worldwide. And there is some evidence to suggest that the pace of transformation and the extent of the disruption to existing industries is increasingly significant – recent investments in 4IR have proven to be able to improve productivity by 15% to 20%, for example.

This change has a number of implications, with two in particular having relevance to global supply chains.

Firstly, increased disruption is likely to prompt existing incumbents to re-assess their broader business models. Deciding whether or not to re-locate operations or re-engineer a supply chain is time consuming and difficult. However, if firms are already reconsidering their global footprint, then it creates an opportunity for destinations to enter a re-engineered global value chain.

Secondly, changes to industries are also changing what makes a destination attractive for that sector and the relative importance of different endowments. If the way that you make something has changed, then what you look for in a destination will change too.

For example, it has been the case historically that a highly skilled workforce has been a key competitive advantage in manufacturing – particularly more advanced manufacturing sectors such as automotive. In other areas of manufacturing, the availability of reliable low-cost labour has been a key determinant.

However, it is likely that as automation increases in the manufacturing sector, the advantage provided by a plentiful supply of low-cost labour or particular skills that can be automated is likely to decrease relative to other advantages.

Potential Implications:

- New drivers of investment will emerge: Destinations that have the resources and infrastructure that can support automation – for example, high 5G connectivity, or a trained engineering workforce – will be able to position themselves to emerge as leaders in sectors in which they may not yet be competing.

- Digitalisation of trade will grow in potential and importance: While technology has the potential to ease global supply chains and address bottlenecks, the challenge is often regulatory as much as technological. The Covid-19 pandemic saw some digitalisation in order to enable trade to continue – countries that can accelerate digitalisation (or which can construct new common international standards) have the potential to set themselves apart.

- Need to pivot for some locations: Economies that have competed on the basis of low-cost labour are likely to see that advantage eroded as the cost of automating that labour falls. In order to continue to compete, these countries will need to pivot to a articulate a broader rationale for their competitiveness.

3. The increasing centrality of climate change

While climate change and the drive to reduce emissions is not a new challenge, it is having an increasingly direct impact on investor decision making – with emissions now a key consideration for many.

As governments look for further ways to drive down emissions – including regulatory routes such as the EU’s Carbon Border Adjustment Mechanism – it is likely that emissions will become an increasingly binding constraint on firms’ costs.

Likewise, as ESG credentials become an important aspect of how capital is allocated – whether through the growth of ESG-specific funds or the increased prominence of emissions as a risk factor – it is likely that the importance placed on emissions will continue to take a more prominent role in decision making.

These factors are likely to be particularly relevant in FDI, where investment decisions are often made over a long time horizon. Investors may need to assess what the likely pressure will be on their emissions not only today, when a decision to build a industrial plant is made, but also in five years’ time when the plant opens.

The impact of this is likely to be that emissions move from being a matter of good corporate citizenship to being an increasingly binding constraint on firms’ operating costs and ability to access capital.

Potential Implications:

- Clean energy will become an important differentiator: Destinations that offer plentiful availability of reliable, low-cost green energy will provide firms with the ability to ‘green’ their supply chains. Given still limited availability currently of green energy, what will be important is not only existing capacity but investment plans to develop capacity in the near future.

- Emissions targets may drive shorter supply chains in some sectors: According to the WTO, international trade is estimated to represent 20 to 30 percent of global emissions, and in some sectors transportation accounts for more emissions than production – as much as 80 percent in some sectors. In those sectors where transportation is a major determinant of total emissions, it is likely that more binding emissions targets will ramp up the pressure on firms to find ways to cut emissions from their supply chains. In turn, countries that are located close to key markets in the value chain, and can therefore reduce the emissions created through transportation, may be able to position this as a competitive advantage.

Maximising the impact of global value chains

Global value chains are the processes by which services, materials, parts and components cross borders multiple times to create a final product.

As well as being central to modern manufacturing, they are also a key element in international trade. While popular discussion tends to focus on trade in finished goods, according to the OECD, around 70 percent of trade worldwide involves global value chains.

Global value chains have helped to transform how products and, to a lesser degree, services are created and delivered. They mean that multinational companies are able to structure their operations in a way that maximises the advantages of different locations.

In practice, a global value chain could include designing and marketing a product in one country, sourcing raw materials from two different countries and components from another, semiconductor chips from a fifth country and assembling the product in a sixth.

This process has helped to drive down costs by making production more efficient.

As well as benefitting businesses, global value chains have also created opportunities for countries around the world. They have meant that countries are able to capture parts of the value chain in industries which fit the advantages they provide.

For example, a country with limited access to capital and technology may still be able to participate in global value chains for highly specialised products by, for example, providing low cost labour in manufacturing parts which are assembled elsewhere.

Countries also have the opportunity to generate more value by moving up the value chain in a particular area of expertise (for example, moving from just manufacturing car wheels to manufacturing and designing car wheels) or by moving horizontally (for example, moving from manufacturing car wheels to manufacturing wheels for cars and planes).

Connecting global value chains to local economies

As with foreign direct investment more generally, global value chains provide value both directly and indirectly.

The direct benefits are clear – they provide capital, create jobs and support the development of exports. They can also help to support the wider development of links with other economies by strengthening trade ties.

But the indirect benefits of global value chains are also important. Research suggests that linking local economies with global value chains can have positive effects elsewhere in the economy. It also suggests that this effect is stronger when the link to the global value chain comes through FDI rather than more arm’s length sourcing.

When elements of global value chains are located in a country, the higher technical expertise and technology can create benefits for the rest of the economy. For example, employees working within the value chain of a multinational company are likely to learn new techniques and bring those techniques with them when they move jobs to work for a local business.

However, it is important to note that these benefits are not only derived from FDI inflows as international firms invest in an economy, but can be derived from FDI outflows as local firms invest internationally too. In Harnessing Global Value Chains for Regional Development, Riccardo Crescenzi and Oliver Harman highlight the example of CEMEX. They note that CEMEX’s international investments – particularly in advanced economies such as Spain – helped it to learn new processes that it was able to integrate into its operations back in its home market in Mexico.

But these spillover effects are not predetermined. While they may seek some partnerships to develop local supply chains, multinational companies will often seek to minimise spillovers and knowledge transfer in order to maintain competitive advantage.

Maximising the impact that global value chains can have within an economy requires active engagement and incentives from governments. IPAs in particular – given their close links with existing and potential investors – can have an important role to play in working with multinationals and ensuring that the full potential of global value chains is realised.

About the author

Duncan Mayall

Director – Integrated Government Specialist

Duncan has over 15 years of experience in government and corporate advisory. He specialises in economic analysis and its application to policy and communications, focusing on FDI and sovereign wealth funds.

He has worked on economic communications campaigns for governments, including Bahrain, Saudi Arabia, Iraq, and Morocco. Before this, Duncan worked in financial communications, advising several listed businesses – from FTSE100 to AIM listed companies – and working across various corporate transactions.